What is the Reliable Audit Trail (Piste d’Audit Fiable) ?

The PAF is one of the three dematerialization processes accepted by the legislator and which is specific to France. The Reliable Audit Trail is an internal documentation that explains and proves the invoicing process.

In all cases, the starting point of the reliable audit trail must correspond to the starting point of the billing process.

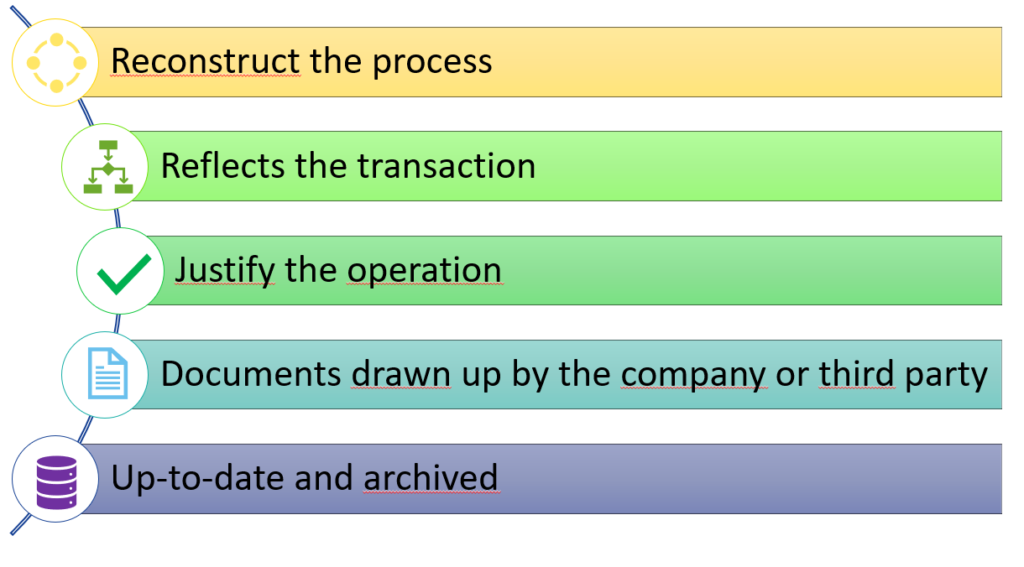

The audit trail must allow:

- Reconstruct, in chronological order, the entire invoicing process

- Ensure that the invoice issued or received reflects the transaction that took place

- To justify any operation by a piece.

The audit trail may consist of documents drawn up by the company itself (quotation, purchase order) or by third parties (account statements).

The audit trail must correspond to the purchases/services that took place. For example, the purchase order must correspond to an order really

It is considered reliable when the administration can establish the link between the supporting documents and the operations carried out.